Getting fast access to cash without paperwork or hidden fees is easier when you already bank with HSBC.

The Quick Loan gives eligible customers a way to borrow up to £25,000 with no arrangement charges, instant decisions, and clear fixed payments.

It’s a straightforward option for short-term needs, emergency expenses, or flexible projects, delivered entirely online.

What an HSBC Quick Loan Delivers

Gain rapid access to unsecured cash while locking in a fixed rate and clear schedule.

HSBC lets you borrow £1,000 – £25,000 (up to £50,000 for long-standing customers) with terms lasting one to eight years. Decisions arrive almost instantly once HSBC verifies your details.

Key advantages:

- Predictable costs: fixed APR keeps monthly figures stable

- No arrangement fees: every pound borrowed goes toward your goal

- Early-repayment freedom: overpay anytime without penalty

- Worldwide reach: similar quick-decision products exist in most HSBC markets, although limits and rates differ locally

Representative 6.4 % APR applies to loans between £7,500 and £20,000 in the United Kingdom.

HSBC Quick Loan vs Regular Personal Loan

Pick the product that respects your timeline and relationship with the bank.

| Feature | Quick Loan (existing current-account holders) | Standard HSBC Personal Loan (all applicants) |

| Application route | Online banking or mobile app only | Online, branch, or phone |

| Decision speed | Usually within seconds | 2 – 5 working days for newcomers |

| Amount | £1,000 – £25,000 | £1,000 – £25,000 (up to £50,000 for established clients) |

| Fees | None | None |

| Suitable when | Immediate funds, emergency repairs, travel, medical bills | Longer planning horizon or borrowing above quick-loan cap |

A quick loan suits urgent expenses and confident budgets, while the standard product fits larger or planned projects.

Confirming Eligibility in the United Kingdom

Save time by checking baseline requirements before applying.

| Criterion | Typical Quick-Loan Requirement | Why It Matters |

| Age | 18 + | Legal borrowing age |

| Residency | Resident in lending country (UK example) | Enables credit checks |

| Income | £10,000 + taxable annual income or equivalent | Demonstrates repayment capacity |

| Current account | Active HSBC current account for at least one salary cycle | Allows instant fund transfer |

Outside the United Kingdom, local minimum income, residency, and account tenure rules may vary, so review your regional HSBC site.

How Much You Can Borrow: Using the Calculator

Estimate a realistic figure in minutes.

- Open the HSBC loan calculator through online banking or the public site.

- Enter net monthly income and essential outgoings. Include rent, utilities, and existing debt.

- Select the desired amount and term. The tool refreshes to show an estimated monthly repayment and total interest.

- Adjust figures until repayment sits comfortably below discretionary income.

- Save or print the illustration to compare later against the formal offer.

Consistent numbers help HSBC’s automated system approve you faster.

Current Interest Rates and Fees Explained

HSBC publishes a representative APR, allowing you to easily benchmark costs. For mid-sized loans (UK example), the advertised 6.4 % APR covers £7,500 – £20,000, although rates may reach 22.9 % if credit history is weaker.

Charges you will not face: arrangement fees, setup costs, or hidden insurance add-ons.

You may incur up to two months’ extra interest if you repay the entire balance early; however, regular overpayments remain penalty-free, significantly reducing total interest.

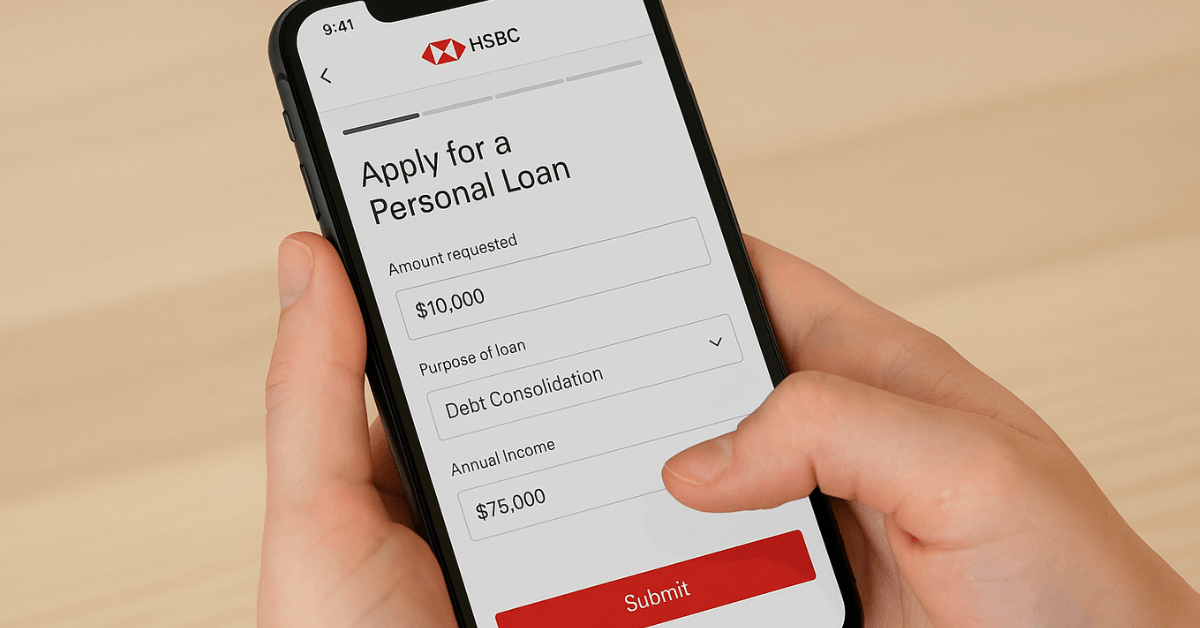

Step-by-Step Application Process

Follow this order to avoid missing information and triggering delays.

- Log in to online banking or the HSBC UK app.

- Navigate to “Loans.” Choose Quick Loan.

- Run the calculator again if you have not done so in the last 24 hours.

- Complete personal details (full name, date of birth, marital status, dependents, postcode).

- State employment and income precisely; uploads may be skipped if HSBC already holds recent salary data.

- Identify loan purpose from the drop-down list; choose “Other” only when no category matches.

- Review the summary for accuracy, then submit.

- Wait for an on-screen decision. Most applicants receive an answer within seconds.

- Electronically sign the credit agreement.

- Receive funds typically within minutes, though rare security checks can extend this to one working day.

Required Documents Checklist

Have digital copies ready to speed compliance calls.

- Government-issued photo ID (passport or driving licence)

- Latest payslip or the last three months of bank statements showing salary

- Proof of address dated within ninety days (utility bill or council tax)

- Existing loan or credit-card statements if consolidating debts

- Many long-time HSBC clients bypass uploads because their internal records already meet regulatory requirements.

Smart Tips for Approval

Strengthen your profile before pressing “Apply.”

- Tidy your credit report by correcting errors and paying small balances first.

- Keep utilisation below 30 % on revolving credit.

- Reduce overdraft reliance during the three months leading up to the application.

- Avoid simultaneous finance applications that scatter hard inquiries across your file.

- Borrow only what solves the issue; larger sums can trigger manual underwriting.

These moves can win a lower rate and a smoother experience.

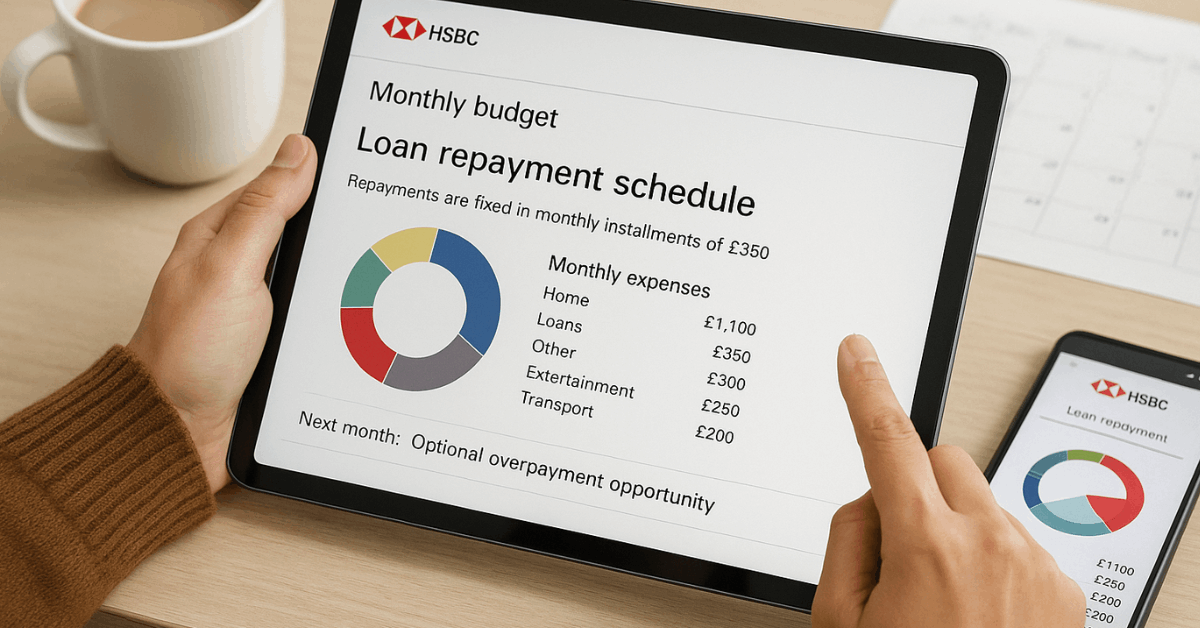

Repayment Options and Early Pay-Off Strategies

HSBC offers monthly direct debits on fixed dates. You may:

- Round up the instalment to the next £10 to cut interest silently.

- Drop a lump-sum overpayment after the annual bonus arrives.

- Synchronize the payment date with the salary to reduce missed payment risk.

Early settlement saves interest; confirm any remaining fee (normally up to 58 days’ interest) so you can calculate net benefit.

Pros and Cons at a Glance

Advantages:

- Immediate decision for current-account holders

- Predictable costs through fixed APR

- Global brand reputation supports trust worldwide

- No collateral required

Drawbacks:

- Non-customers face slower approval and potential lower caps

- Strong credit still needed for headline rate

- Loans above £25,000 move to the standard product, losing “quick” speed

HSBC vs Other Quick-Decision Lenders (United Kingdom Snapshot 2025)

| Lender | Representative APR | Amount Range | Term Range | Key Edge |

| HSBC | 6.4 % (7.5k–20k) | £1k–£25k | 1–8 yrs | Online decision; no fees |

| TSB | 5.9 % (7.5k–25k) | £1k–£50k | 1–7 yrs | Two repayment-holiday option |

| M&S Bank | 6.0 % | £1k–£25k | 1–7 yrs | Joint-application feature |

| Santander | 6.0 % | £1k–£25k | 1–5 yrs | Fast branch support |

Rates above reflect UK data mid-2025; worldwide figures differ, so always check local HSBC and competitor sites before committing.

Contact and Support

Here’s how to get help or loan details directly from HSBC, no matter where you're located.

- Customer service worldwide: Start with local HSBC phone or chat inside the app.

- United Kingdom helpline: 03457 404 404 (personal) | 03457 707 070 (Premier)

- Mail: HSBC UK Bank plc, 1 Centenary Square, Birmingham B1 1HQ, United Kingdom

- The global website, hsbc.com, redirects you to regional pages for country-specific quick loan information.

Conclusion

An HSBC Quick Loan offers speed, transparency, and flexibility when unforeseen costs appear.

By confirming eligibility, fine-tuning the loan amount with the calculator, and following the structured application path above, you position yourself for near-instant funding and manageable repayments.

Compare rates worldwide, borrow only what advances your goal, and overpay whenever cash flow allows to pay off debt sooner and finish debt-free.